Circle's Acquisition of Axelar Sparks Controversy: AXL Plunges 15% as Long as People Don't Want Coin

Original Article Title: "Circle's Acquisition of Axelar Sparks Controversy: Giant Only Wants People, Not Coin"

Original Article Author: Azuma, Odaily Planet Daily

In the early morning of December 16th, stablecoin giant Circle officially announced that it has completed the signing of an agreement to acquire the core team and technology of Interop Labs, the initial development team of the cross-chain protocol Axelar Network. This move is intended to advance Circle's cross-chain infrastructure strategy and support Circle in achieving seamless and scalable interoperability on its core products such as Arc and CCTP.

This was supposed to be another typical case of an industry giant acquiring a high-quality team, seemingly a win-win situation. However, the key issue lies in the fact that Circle explicitly mentioned in the acquisition announcement that this transaction only involves the Interop Labs team and its proprietary intellectual property, while Axelar Network, the Axelar Foundation, and the AXL token will continue to operate independently under community governance. The other contributing team of the original project, Common Prefix, will take over the relevant activities of Interop Labs.

In simple terms, Circle took away Axelar Network's original development team but explicitly excluded Axelar Network itself and its token AXL.

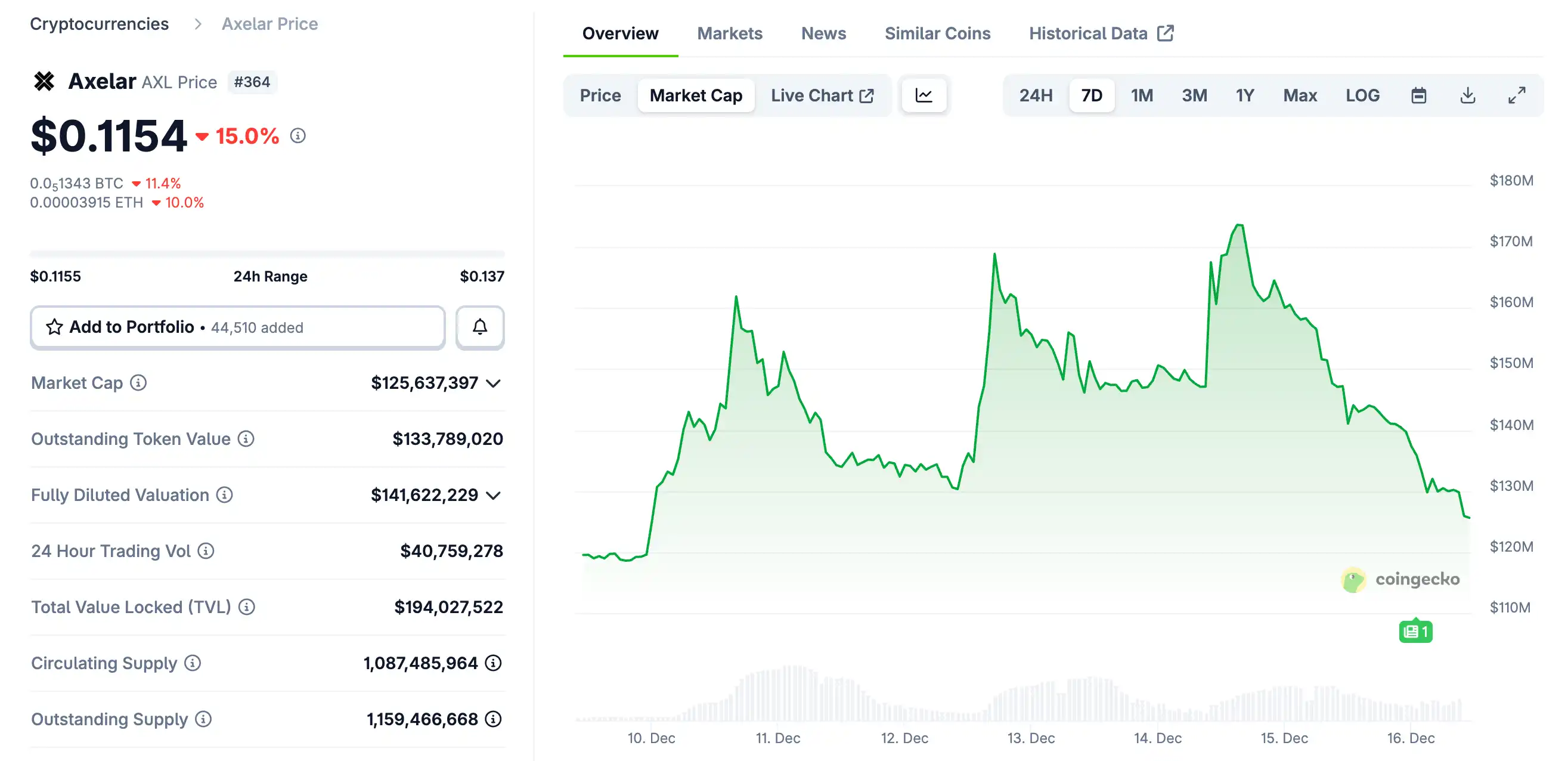

Impacted by this sudden news, AXL experienced a sharp drop, trading around $0.115 as of approximately 10:00 AM this morning with a 24-hour decline of 15%.

At the same time, the unique situation of the acquisition itself, characterized by "wanting people but not coin," and the ensuing "Equity vs. Token" issue, has sparked numerous discussions within the community, with proponents and opponents of this type of acquisition model holding differing views and engaging in heated debates.

Opposing Viewpoint: Implicit RUG, Chaos by Circle, Only Token Holders Are Hurt

A key force within the opposing camp consists of some VCs, which is not hard to understand—"I invested real money in the project's token equity, held a substantial amount of the token, and now you take away the ones doing the work - what good is this token to me?"

Simon Dedic, Founder of Moonrock Capital, commented on this: "Another acquisition, another RUG. Circle acquires Axelar but explicitly excludes the foundation and AXL token, this is simply a criminal act. Even if it does not violate the law, it goes against ethics. If you are a founder looking to issue a token: either treat it like equity or get lost."

The Block Co-founder and 6MV Founder Mike Dudas commented, "For those who think this is a token vs. equity issue, I can tell you definitively that this is all Circle's doing. There are rumors that Circle's VP of Corporate Development once told a co-founder of Axelar, 'I don't care about your investors,' and without paying any consideration to investors, 'bought' the CEO and IP out from under them, which are crucial to Arc's launch."

Lombard Finance Founder posted Axelar's trend and predicted, "Axelar's core team has been bought by Circle, and AXL may now be worthless. The token has been issued for over three years, the team's equity has already been fully cashed out. Yet, the result is very uncomfortable: the team and/or investors sold tokens for profit, while token holders can only hope for a distant dream."

ChainLink community figure Zach Rynes stated, "This once again exposes the token vs. equity conflict of interest issue plaguing the crypto industry. The development team behind the protocol has been successfully acquired, while token holders who funded that team have received nothing. The so-called continued independent operation under community governance is no different from the development team abandoning users for a better future. If we want to attract real capital, this is the industry's top issue that needs to be addressed."

SOAR Ecosystem Lead Nicholas Wenzel said, "The Axelar token is heading towards zero, thanks for participating. This is another case of token holders gaining nothing while equity holders profit handsomely from the acquisition."

Supporting Viewpoint: Normal Market Behavior, Tokens are inherently at the bottom of the capital structure

If the opposing side focuses more on the unfair treatment of token holders, the supporting side will focus more on the market rules of financing and M&A.

Arca Chief Investment Officer Jeff Dorman believes Circle's actions are fair and explains in detail the capital structure of corporate financing and the natural disadvantage tokens find themselves in.

Businesses raise funds through different levels of the capital structure, and these levels inherently have a clear priority order, with some levels naturally ahead of others — secured debt > unsecured senior debt > subordinated debt > preferred shares > common shares > tokens.

Throughout history, there have been countless cases where the interests of one type of investor have been achieved at the expense of another type of investor.

· In bankruptcy liquidation, creditors succeed at the expense of equity investors;

· In leveraged buyouts (LBOs), equity holders often profit at the expense of debt holders;

· In take-unders, creditors usually have priority over equity holders;

· In strategic acquisitions, both creditors and equity holders usually benefit (but not always);

· And tokens are often at the bottom of the capital structure…

This does not mean that tokens have no value, nor does it mean that tokens necessarily need some kind of "protective mechanism," but the market needs to recognize a reality: when a company acquires another company of already low value, and the tokens issued by that company are virtually worthless, token holders will not magically receive a "unicorn dividend." In such cases, equity returns are often achieved at the expense of token losses.

Avichal Garg, Co-Founder of Electric Capital, also commented: "This is a normal phenomenon. If all future value is created by the team, then there is no company willing to pay returns to investors."

Core Contradiction: What Exactly Are Tokens?

Amid the "talent over tokens" acquisition controversy between Axelar and Circle, both sides of the debate seem to have valid points.

The anger of the opposition is real: Token holders took on risk at the project's most challenging and critical liquidity and narrative support stage, only to be completely excluded at the key value realization point. From the outcome perspective, the core team and intellectual property have achieved value realization, while the tokens have been left in a narrative vacuum of "community governance," and the market has provided the most direct vote through price, which has indeed left all believers in token value deeply frustrated.

The judgment of the supporters also has practical rationality: From a strict capital structure standpoint, tokens are neither debt nor equity, naturally lacking priority in the context of mergers and liquidations. Circle did not violate existing business rules; it simply made a calculated decision based on the assets most valuable to itself.

The true core of the contradiction lies not in whether Circle is ethical, but in an issue that has long been deliberately avoided by the industry: What exactly is a token in the legal and economic structure?

During optimistic times, tokens were assumed to be "quasi-equity," endowed with the imagination of claiming success in the future; however, in real scenarios such as mergers and acquisitions, bankruptcy, and liquidation, they were quickly reduced to their original form of "non-equity instruments." This narrative-based equity and the underlying structure are the root causes of the repeated conflicts.

The Axelar acquisition case may not be the last of such controversies, but hopefully, it can serve as an opportunity for the industry to further contemplate the positioning and significance of tokens—Tokens do not inherently possess rights; only rights that have been institutionalized and structured will be recognized at crucial moments. The specific implementation still requires all industry participants to explore and practice together.

You may also like

WEEX API Fast Connect: Turn Every Sign-In Into a Live Trader in Under 10 Seconds

WEEX API Fast Connect is a one-click OAuth authorization system that lets your users link their WEEX account without ever touching an API key. Frictionless onboarding, faster conversions, higher retention — built for WEEX Broker partners.

From Le Mans to the Rollercoaster: Carl Moon Takes On Portimão

Crypto world renowned KOL and racing driver Carl Moon, backed by WEEX, heads to the Ferrari Challenge Portugal round at the Algarve International Circuit, July 16–19, fresh off a podium finish at Le Mans. Here's why this race is one to watch.

Fast execution. Split-second accuracy. Security that never blinks. That's WEEX — and that's exactly how Carl races.

The Downfall of a Public Company: A $1.46 Billion Bet on WLFI, $540 Million Went to the Trump Family

Dragonfly Partner: BTC is Intergenerational Wealth, Optimistic About ETH and SOL

Goldman Sachs Calls to Go Long on Chinese AI: $4 Trillion Market Value Behind, Global Funds Only Allocated 1.2%

The New Landscape of Cryptocurrency in Europe: Why Germany Takes Center Stage?

Robinhood vs xStocks: Stock Tokenization Shouldn't Just Focus on Ticker On-Chain

Nexo launches crypto card in Argentina as Latin America push grows

Bank of America: Nvidia's Forward P/E Falls to 7-Year Low, Market Paying for a Non-Existent Risk

Q2 2026 CEX Trading Data Review: Who's Slacking Off? Who's Inflating Their OI?

Kraken leads MiCA exchanges as EU crypto rules bite

Is the Frenzied Acquisition of Crypto Companies by Giants Good or Bad?

Wall Street Morning Briefing: US-Iran Ceasefire Agreement Collapses, Oil Rises to $80, Nasdaq Gains While Dow Drops

The 'MEV Moment' in Market Predictions: Betting on Ups and Downs or Creating Them

Can SK Hynix Save the Semiconductor Industry with Sevenfold Oversubscription?

The End of the 'Easy Money' Era for AI Semiconductors: Beware of the 'Ghost Stories' Unfolding

Trump Earns $2.2 Billion Annually, Two-Thirds from Cryptocurrency, Averaging 87 Stock Trades Daily

Before the Sea Temperature Rises, the K-Line Warms Up First—A Comprehensive Projection of the 2026 El Niño in Cryptocurrency

WEEX API Fast Connect: Turn Every Sign-In Into a Live Trader in Under 10 Seconds

WEEX API Fast Connect is a one-click OAuth authorization system that lets your users link their WEEX account without ever touching an API key. Frictionless onboarding, faster conversions, higher retention — built for WEEX Broker partners.

From Le Mans to the Rollercoaster: Carl Moon Takes On Portimão

Crypto world renowned KOL and racing driver Carl Moon, backed by WEEX, heads to the Ferrari Challenge Portugal round at the Algarve International Circuit, July 16–19, fresh off a podium finish at Le Mans. Here's why this race is one to watch.

Fast execution. Split-second accuracy. Security that never blinks. That's WEEX — and that's exactly how Carl races.