Ethereum's Identity Crisis: Cryptocurrency or Bitcoin's Shadow?

Original Article Title: The ETH Debate: Is it Cryptomoney?

Original Article Author: @AvgJoesCrypto, Messari

Translation: Luffy, Foresight News

Among all mainstream cryptocurrency assets, Ethereum has sparked the most intense debate. While Bitcoin has been widely recognized as the leading cryptocurrency, Ethereum's position has always been in question. To some, Ethereum is seen as the only credible non-sovereign monetary-like asset apart from Bitcoin; while others believe Ethereum is fundamentally a business that has seen declining revenues, tightening profit margins, and faces fierce competition from many other public chains offering faster transactions and lower costs.

This debate seemed to reach its peak in the first half of this year. In March, Ripple (XRP) briefly surpassed Ethereum in fully diluted valuation (notably, all Ethereum tokens are in circulation, while only about 60% of Ripple's total supply is circulating).

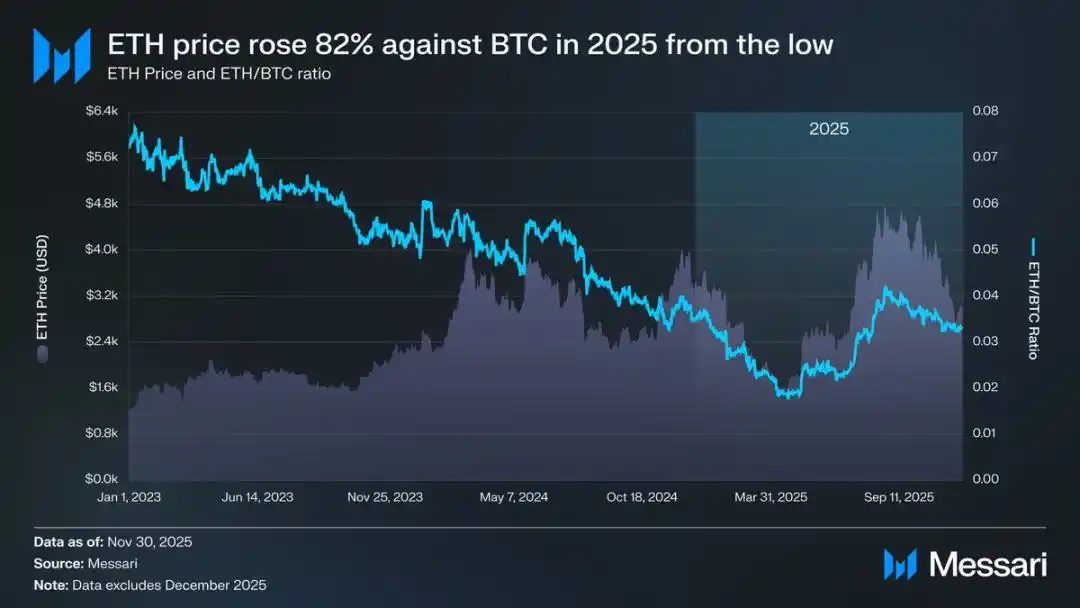

On March 16th, Ethereum's fully diluted valuation was $227.65 billion, while Ripple's equivalent valuation reached $239.23 billion. This result was almost unimaginable a year ago. Subsequently, on April 8th, 2025, Ethereum's exchange rate to Bitcoin (ETH/BTC) fell below 0.02, hitting a record low since February 2020. In other words, Ethereum has completely retraced all its gains relative to Bitcoin from the previous bull run. At that time, market sentiment towards Ethereum hit rock bottom.

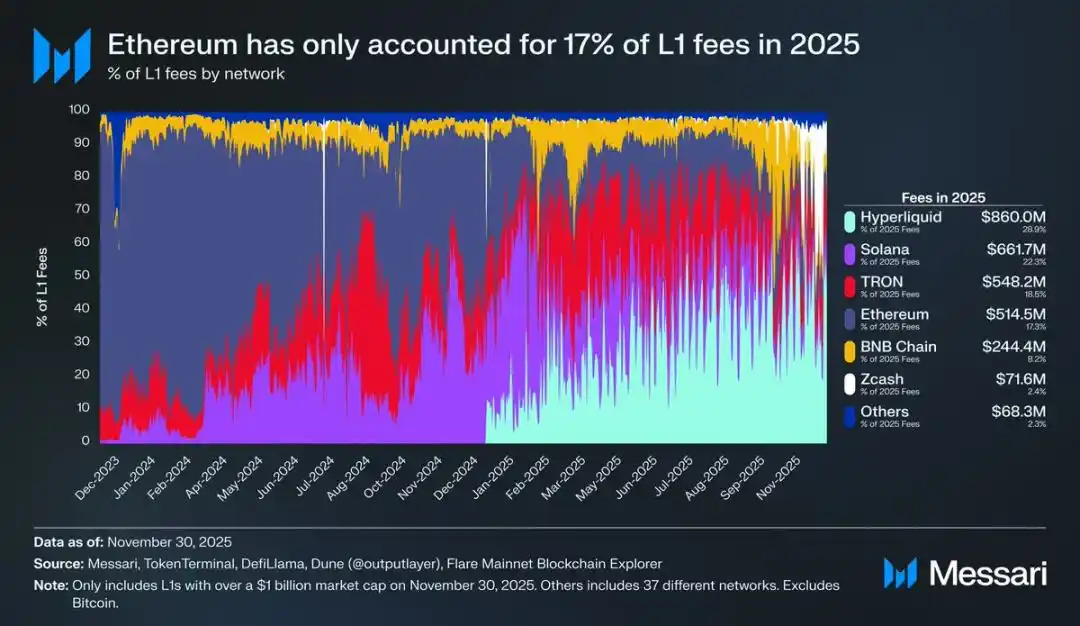

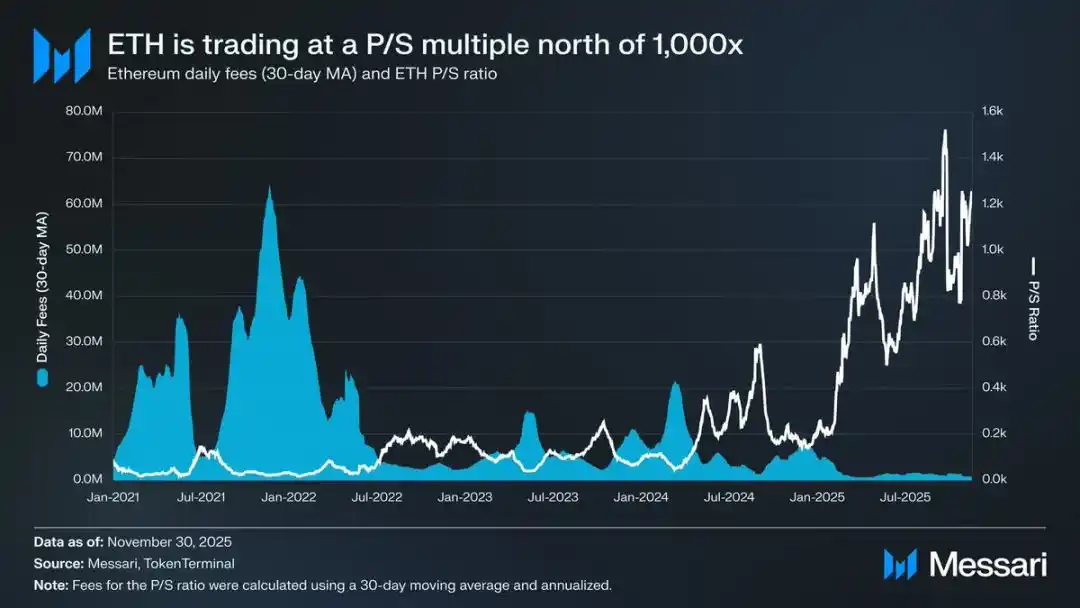

To make matters worse, the price decline was just the tip of the iceberg. As competitors' ecosystems flourished, Ethereum's share of the on-chain fee market continued to shrink. In 2024, Solana made a comeback; in 2025, Hyperliquid emerged. Together, the two pushed Ethereum's fee market share down to 17%, ranking it fourth among public chains—a cliff-like drop from its top spot a year ago. While fees may not tell the whole story, they are a clear signal of economic activity flow. Today, Ethereum is facing the most challenging competitive landscape in its development history.

However, historical experience has shown that significant reversals in the cryptocurrency market often begin at the most pessimistic moment of market sentiment. When Ethereum is pronounced by the outside world as a "failed asset," most of its apparent decline has already been absorbed by market prices.

In May 2025, signs of market overbearishness towards Ethereum began to emerge. It was during this period that Ethereum experienced a strong rebound in both its exchange rate against Bitcoin and its price in USD. The Ethereum-to-Bitcoin exchange rate climbed from a low of 0.017 in April to 0.042 in August, representing a 139% increase. During the same period, Ethereum's USD price surged from $1646 to $4793, marking a 191% increase. This upward trend peaked on August 24th when the price of Ethereum reached $4946, setting a new all-time high. After this reevaluation of value, Ethereum's overall trajectory clearly returned to an upward trend. The Ethereum Foundation's leadership transition and the emergence of a group of treasury companies focused on Ethereum injected confidence into the market.

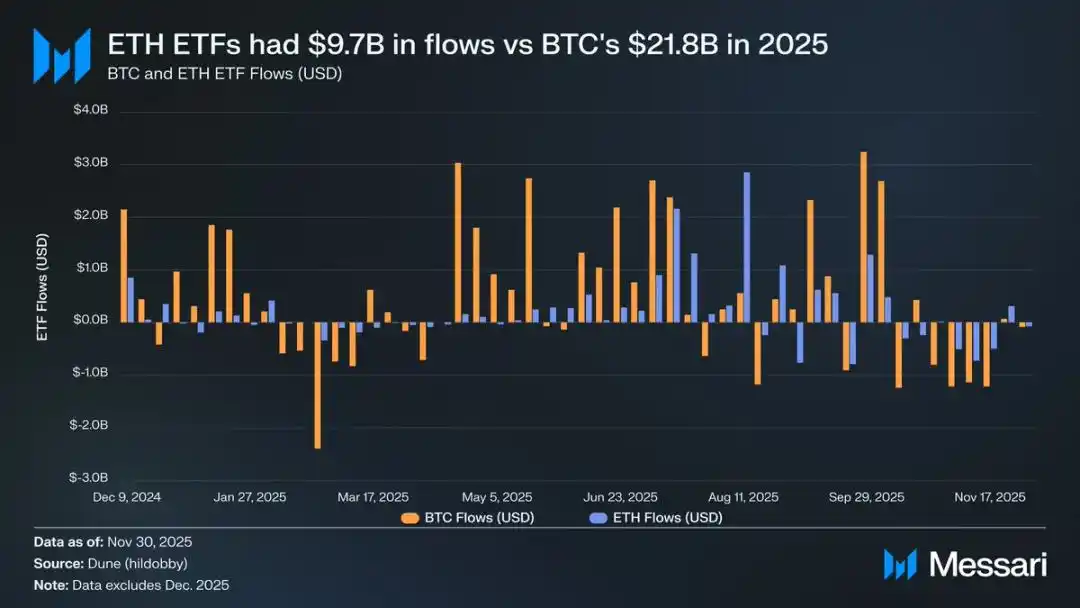

Prior to this round of growth, the diverging fortunes of Ethereum and Bitcoin were vividly reflected in the exchange-traded fund (ETF) markets for both. In July 2024, an Ethereum spot ETF was launched, but its fund inflows were very weak. In the first six months post-listing, its net inflow was only $2.41 billion, showcasing a stark contrast to the record-breaking performance of the Bitcoin ETF.

However, with Ethereum's strong recovery, concerns about its ETF fund inflows dissipated. Looking at the entire year, the net inflow of the Ethereum spot ETF reached $9.72 billion, while the Bitcoin ETF reached $21.78 billion. Considering that Bitcoin's market cap is nearly five times that of Ethereum, the disparity in the scale of ETF fund inflows is only 2.2 times, much lower than market expectations. In other words, when adjusted for market cap size, the market demand for Ethereum ETFs actually exceeds that of Bitcoin. This result completely reversed the narrative that "institutions lack genuine interest in Ethereum." Moreover, during specific time periods, the inflow of funds into the Ethereum ETF even surpassed Bitcoin directly. From May 26th to August 25th, the net inflow into the Ethereum ETF was $10.2 billion, exceeding the $9.79 billion for the Bitcoin ETF during the same period, marking the first clear tilt of institutional demand towards Ethereum.

Looking at the performance of ETF issuers, BlackRock continued to lead the market. By the end of 2025, BlackRock's Ethereum ETF holdings reached 3.7 million ETH, representing 60% of the Ethereum spot ETF market share. Compared to the year-end 2024 holding of 1.1 million ETH, this marked a 241% increase, with an annual growth rate far exceeding other issuers. Overall, the Ethereum spot ETF's holdings at the end of 2025 were 6.2 million ETH, accounting for approximately 5% of its total token supply.

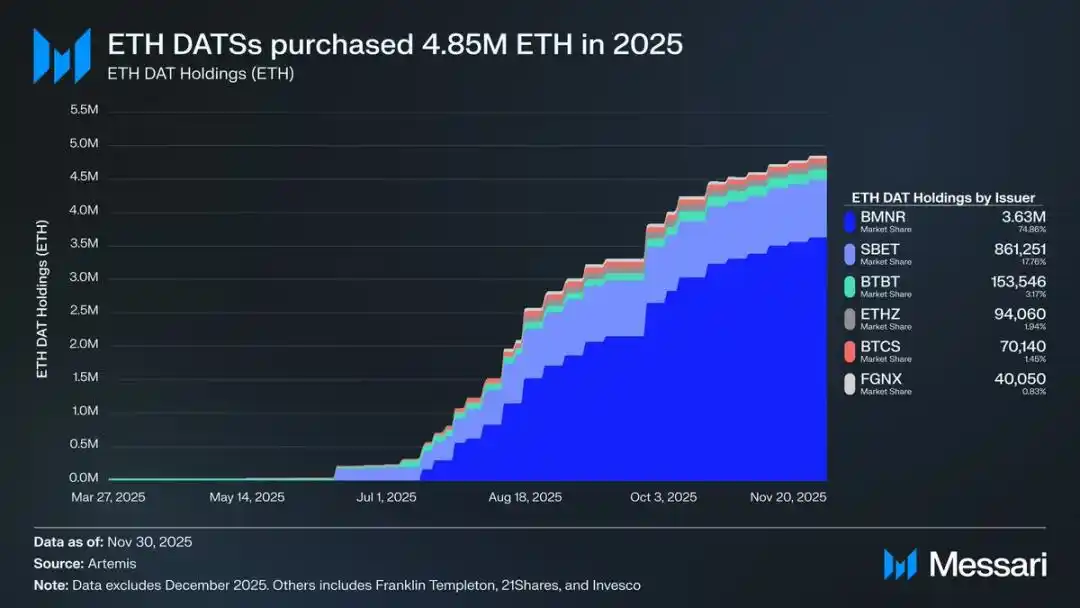

Behind Ethereum's strong rebound, the key driver has been the rise of Ethereum treasury companies. These reserve vaults have created unprecedented stable and sustained demand for Ethereum, providing support that narrative-driven or speculative funds cannot match. If Ethereum's price action marks a clear inflection point, then the continued accumulation by treasury companies represents a profound, structural shift that brought about this turning point.

By 2025, Ethereum treasury companies had accumulated 4.8 million Ethereum, representing 4% of its total supply, significantly impacting Ethereum's price. Among them, the most prominent performer is Bitmine led by Tom Lee (stock code BMNR). This company, originally focused on Bitcoin mining, began converting its reserve funds and capital to Ethereum in July 2025. From July to November, Bitmine acquired a total of 3.63 million Ethereum, holding 75% of the market share in the Ethereum treasury company market.

Despite Ethereum's strong rebound, the upward momentum eventually cooled off. As of November 30, Ethereum's price had retraced from its August high to $2,991, even lower than the previous bull market's peak of $4,878. While Ethereum's situation has significantly improved from its April low, this round of rebound has not completely dispelled the structural concerns that initially triggered market pessimism. On the contrary, the controversy surrounding Ethereum's positioning is once again in the public eye with even more intensity.

On one hand, Ethereum is exhibiting many features similar to Bitcoin, which are key to Bitcoin's ascent as a monetary asset. Today, Ethereum ETF inflows are no longer weak, and the Ethereum treasury company has become a source of its sustained demand. Perhaps most importantly, an increasing number of market participants are starting to differentiate Ethereum from other altcoins, incorporating it into the same monetary framework as Bitcoin.

On the other hand, the core issues that dragged Ethereum down in the first half of this year have yet to be resolved. Ethereum's core fundamentals have not fully recovered: its share of the public chain transaction fee market continues to be squeezed by strong competitors like Solana and Hyperliquid; the transaction activity on the Ethereum base layer is still far below the peak levels of the previous bull market; despite a significant price rebound, Bitcoin has easily surpassed its all-time high, while Ethereum is still lingering below its all-time high. Even in Ethereum's strongest months, there are still many holders who see this rally as an opportunity to cash out rather than a recognition of its long-term value.

The core issue of this controversy is not whether Ethereum has value, but how the asset ETH can accumulate value from the development of the Ethereum network.

In the previous bull market, the market widely believed that ETH's value would directly benefit from the success of the Ethereum network. This is the core logic of the "Sound Money Thesis": the utility of the Ethereum network will drive a significant demand for token burning, thereby establishing a clear and mechanized value support for Ethereum assets.

Today, we can almost certainly say that this logic will no longer hold. Ethereum's fee revenue has plummeted significantly and shows no signs of recovery; meanwhile, the two core areas driving Ethereum network growth — Real-World Assets (RWAs) and the institutional market — settle in USD as their core settlement currency, not in Ethereum.

The future value of Ethereum will depend on how it can indirectly benefit from the development of the Ethereum network. However, this indirect value accumulation carries great uncertainty. Its premise is that as the systemic importance of the Ethereum network continues to rise, more and more users and capital are willing to see Ethereum as a cryptocurrency and store of value tool.

Unlike direct, mechanized value accumulation, this indirect path has no certainty whatsoever. It relies entirely on market social preferences and collective consensus. Of course, this is not a flaw in itself; but it means that Ethereum's value growth will no longer have a necessary causal relationship with Ethereum network economic activity.

All of this will bring Ethereum's controversy back to its most core contradictory point: Ethereum may indeed be gradually accumulating a monetary premium, but this premium always lags behind Bitcoin. The market once again sees Ethereum as a "leverage expression" of Bitcoin's currency attributes rather than an independent monetary asset. Throughout the year 2025, Ethereum's 90-day rolling correlation with Bitcoin remained between 0.7 and 0.9, with the rolling beta coefficient skyrocketing to multi-year highs, briefly exceeding 1.8. This means that Ethereum's price volatility far exceeds Bitcoin's, but it is also always attached to Bitcoin's trend.

This is a subtle yet crucial distinction. The currency attributes that Ethereum possesses today are still recognized by the market as rooted in Bitcoin's currency narrative. As long as the market believes in Bitcoin's non-sovereign store of value attributes, some fringe market participants will be willing to extend this trust to Ethereum. Therefore, if Bitcoin's trend remains strong in 2026, Ethereum will also recapture more lost ground.

Currently, the Ethereum treasury company is still in its early stages of development, and its acquisition of Ethereum funds mainly comes from common stock issuance. However, if the cryptocurrency market experiences a new bull market, such institutions may explore more diversified financing strategies, such as borrowing from the strategy of expanding Bitcoin holdings, issuing convertible bonds and preferred stock.

For example, a Ethereum Treasury company like BitMine can finance itself by issuing low-interest convertible bonds and high-yield preferred shares, using the raised funds to directly accumulate Ethereum, while staking this Ethereum to earn ongoing rewards. Under reasonable assumptions, the staking rewards can partially offset the bond interest and preferred share dividend payments. This model allows the treasury to continue accumulating Ethereum using financial leverage when market conditions are favorable. Assuming a full-fledged bull market for Bitcoin in 2026, this "second growth curve" of the Ethereum Treasury company will further strengthen Ethereum's high beta attribute relative to Bitcoin.

Ultimately, the current market pricing of Ethereum's monetary premium is still based on Bitcoin's trajectory. Ethereum has not yet become a standalone currency asset with independent macroeconomic fundamental support; it is merely a secondary beneficiary of Bitcoin's currency consensus, and this beneficiary group is gradually expanding. The recent strong rebound of Ethereum reflects that some market participants are willing to see it as akin to Bitcoin rather than just an ordinary public chain token. However, even during a period of relative strength, market confidence in Ethereum remains closely linked to Bitcoin's narrative of continued strength.

In summary, while Ethereum's narrative of monetization has moved beyond its fractured state, it is far from settled. In the current market structure, combined with Ethereum's high beta attribute relative to Bitcoin, as long as Bitcoin's currency narrative continues to play out, Ethereum's price is poised for significant gains. The structural demand from Ethereum Treasury companies and corporate funds will provide tangible upward momentum. However, ultimately, in the foreseeable future, Ethereum's monetization process will still be tied to Bitcoin. Unless Ethereum can achieve a low correlation and low beta coefficient with Bitcoin over an extended period, a goal it has never achieved, Ethereum's premium space will always remain overshadowed by Bitcoin's halo.

You may also like

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.